The recently enacted Tax Cuts and Jobs Act (TCJA) is a sweeping tax package. In our last article, we provided you with an update on the Federal Gift and Estate Tax. While most will not pay a Federal Gift and Estate Tax, nearly everyone pays income tax. To that end, we have prepared a list of comparisons to last year’s income tax rates with charts, and an explanation of which tax benefits have been expanded, reduced or eliminated. Here’s a look at some of the more important parts which impact individuals. Further, as is the case with the estate tax changes, many of the income tax reductions expire on December 31, 2025.

I. CHANGES IN RATES

1) Ordinary Income Tax Rates. Individuals are subject to income tax on “ordinary income,” such as compensation, and most retirement and interest income, at graduated rates that apply to different tax brackets depending on their filing status.

A. New rates. Beginning in 2018, there will still be seven tax brackets for individuals, with reduced rates in each bracket (except for the 35% and 10% brackets, which remained the same).

B. These new tax rates will not affect your tax on the return you file for 2017. However they will immediately affect the amount of your wage withholding and the amount, if any, of stimated tax that you may need to pay. Click here to see if your withholding should change. https://apps.irs.gov/app/withholdingcalculator/index3.jsp

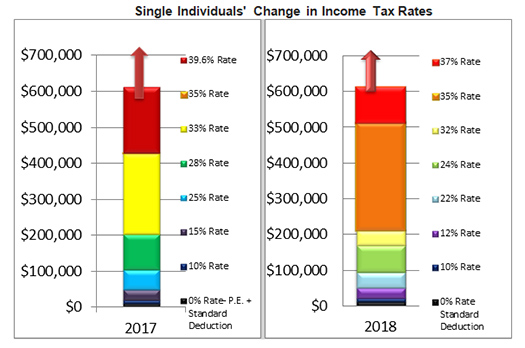

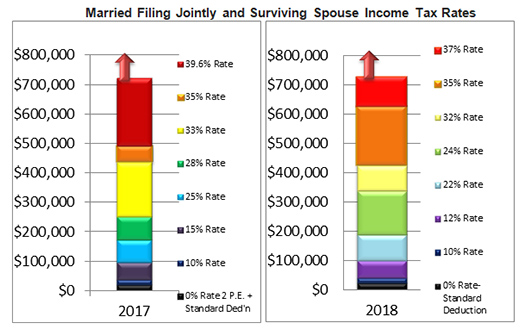

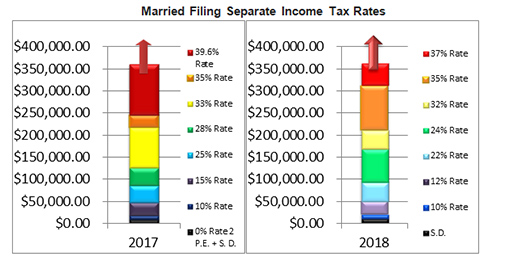

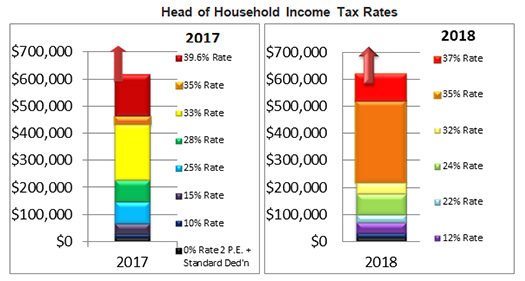

C. Rather than show numbers for each change in bracket, we believe that the charts below provide a good summary and comparison:

D. Surprisingly, when comparing the rates for 2017 and 2018, some individual taxpayers reporting taxable income between $200,000 and $416,700 may actually see an increased effective tax rate. All other individual taxpayers should pay a lower tax rate.

E. Income reported for all brackets in the Married Filing Jointly status will result in a lower tax rate with one small exception. Those reporting taxable income from $400,000 to $416,700 may have a slightly increased tax rate. However, the tax savings from $0.00 to $400,000 far outweigh that increase.

F. The tables for the Married Filing Separately status are very similar to Married Filing Jointly, the only difference being that all of the amounts are cut in half.

G. Again, when comparing the rates for 2017 and 2018, taxpayers filing as head of household who report taxable income between $200,000 and $416,700 may see a small increase in their marginal tax rate. If income is at or near $400,000, the rates provide for at least a $4,000 tax increase.

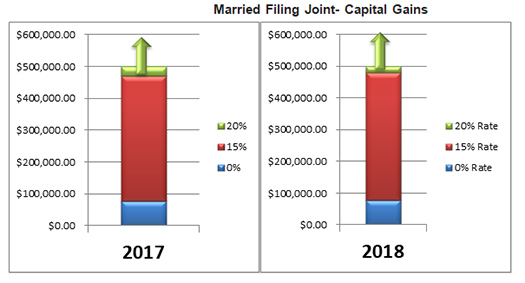

2) Capital Gains. The rates on capital gains and qualified dividends were not changed.

A. Three tax brackets currently apply to net capital gains (including certain kinds of dividends) of individuals and other non-corporate taxpayers. The TCJA, generally, keeps the existing rates and breakpoints on net capital gains and qualified dividends. For example, the chart below illustrates a minor increase in the rate breakpoints for married filing joint persons. Similar small increases also applied to other filing types.

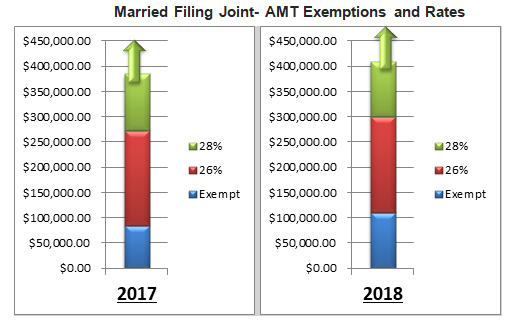

3) Alternative minimum tax (AMT) exemption. A second tax system called the alternative minimum tax (AMT) is designed to reduce a taxpayer’s ability to avoid taxes by using exemptions, deductions and credits. The AMT creates a separate system to calculate income tax without as many exemptions, deductions and credits available under that system. A taxpayer’s total tax liability for the year will be increased by the AMT to the extent the AMT exceeds the normal income tax amount.

A. AMT Exemption Increases. The TCJA increased AMT exemption amounts for tax years 2018 through 2025 to $109,400 for marrieds filing jointly and surviving spouses; $70,300 for single filers; and $54,700 for married couples filing separately. AMT is now less likely to hit at lower income levels. For example, the chart below illustrates the increase in the rate breakpoints for married couples filing jointly:

B. Higher AMT Phaseouts. These increased AMT exemption amounts do not begin to phase out until the taxpayer’s alternative taxable income rises above $1 million for joint returns and surviving spouses, and $500,000 for other taxpayers except estates and trusts.

C. Trust and Estates AMT. For trusts and estates, the base AMT exemption of $22,500 (and phase-out threshold of $75,000) remains unchanged.

D. If you were subject to the individual AMT in the past, you may be able to reduce your wage withholding or pay reduced amounts of estimated taxes going forward due to the exemption increases and higher phase-out levels.

4) Kiddie Tax. The “kiddie tax” rules were simplified. The net unearned income of a child subject to the rules will be taxed at the capital gain and ordinary income rates that apply to trusts and estates, which are higher than individual rates. Thus, the child’s tax will increase, but will be unaffected by the parent’s tax situation or the unearned income of any siblings.

5)Rate Indexing. A related change is that the future annual indexing of all rate brackets (and many other tax amounts) is adjusted for inflation, including AMT and ordinary rates, exemptions and phase-outs. This will help to prevent “bracket creep” and the erosion of the value of a variety of deductions and credits due solely to inflation. Moreover, it will be done in a way that understates inflation more than the current method does. While it won’t be very recognizable immediately, over the years this will push some additional income into higher brackets and reduce the value of many tax breaks.

II. EXPANDED TAX BENEFITS

1) Basis. The TCJA made no substantial changes to the tax-basis rules directly. However, the changes to the Estate Tax have a dramatic effect upon the opportunities to receive a step-up in basis on property received through inheritance. Each estate whose decedent left property with built-in gain will have the opportunity to wipe out the entire built-in gain as of the taxpayer’s date of death, and receive a full step-up in basis up to the fair market value on the date of death. Each decedent who dies in 2018 will be able to transfer a minimum of roughly $11.2 million (indexed for inflation) to the decedent’s successors free of Capital Gains. For a more in depth explanation of how this works, see our article entitled “Trump Tax Cuts & Dramatic Changes to Your Estate Plan”.

2) Overall limitation on itemized deductions. The TCJA suspends the overall limitation on itemized deductions that formerly applied to taxpayers whose AGI exceeded specified thresholds.

3) Child and family tax credit. The TCJA increases the credit for qualifying children (i.e., children under 17) to $2,000 from $1,000, and increases the refundable portion of the credit to $1,400. It also introduces a new (nonrefundable) $500 credit for a taxpayer’s dependents who are not qualifying children. The adjusted gross income level at which these credits begin to be phased out has been increased to $200,000 ($400,000 for joint filers).

4) Standard deduction. The TCJA increases the standard deduction to $24,000 for joint filers, $18,000 for heads of household, and $12,000 for singles and married taxpayers filing separately. Given these increases, many taxpayers will no longer be itemizing deductions. These figures will be indexed for inflation after 2018.

5) Medical expenses. Under the TCJA, for 2017 and 2018, medical expenses are deductible to the extent they exceed 7.5 percent of adjusted gross income for all taxpayers. Previously, the AGI “floor” was 10 percent for most taxpayers.

6) Health care “individual mandate.” Starting in 2019, there is no longer a penalty for individuals who fail to obtain minimum essential health coverage.

III. REDUCED TAX BENEFITS

1)State and local taxes. The itemized deduction for state and local income, real and personal property taxes is limited to a total of $10,000 starting in 2018.

2) Mortgage interest. Under the old rules, an individual could deduct interest on up to a total of $1 million of mortgage debt used to acquire your principal residence and a second home, i.e., acquisition debt. For a married taxpayer filing separately, the limit was $500,000. You could also deduct interest on home equity debt, i.e., debt secured by the qualifying homes. Qualifying home equity debt was limited to the lesser of $100,000 ($50,000 for a married taxpayer filing separately), or the taxpayer’s equity in the home or homes (the excess of the value of the home over the acquisition debt). The funds obtained via a home equity loan did not have to be used to acquire or improve the homes. So you could use home equity debt to pay for education, travel, health care, etc.

A. Under the TCJA, starting in 2018, the limit on qualifying acquisition debt for an individual is reduced to $750,000 ($375,000 for a married taxpayer filing separately). However, for acquisition debt incurred before December 15, 2017, the higher old rule limit applies. The higher old rule limit also applies to debt arising from refinancing pre-December 15, 2017 acquisition debt; to the extent the debt resulting from the refinancing does not exceed the original debt amount. This means you can refinance up to $1 million of pre-December 15, 2017 acquisition debt in the future and not be subject to the reduced limitation.

B. Importantly, starting in 2018, there is no longer a deduction for interest on home equity debt. This applies regardless of when the home equity debt was incurred. Accordingly, if you are considering incurring home equity debt in the future, you should take this factor into consideration. And if you currently have outstanding home equity debt, be prepared to lose the interest deduction for it starting in 2018. (You will still be able to deduct it on your 2017 tax return, filed in 2018.)

C. Lastly, both of these changes last for eight years, through 2025. In the absence of intervening legislation, the pre-TCJA rules come back into effect in 2026. So beginning in 2026, interest on home equity loans will be deductible again, and the limit on qualifying acquisition debt will be raised back to $1 million ($500,000 for married separate filers).

IV. ELIMINATED TAX BENEFITS

1) Miscellaneous itemized deductions. There is no longer a deduction for miscellaneous itemized deductions which were formerly deductible to the extent they exceeded 2 percent of adjusted gross income. This category included items such as tax preparation costs, investment expenses, union dues, and unreimbursed employee expenses.

2) Personal Exemptions. The TCJA eliminates the deduction for personal exemptions. Thus, starting in 2018, taxpayers can no longer claim personal or dependency exemptions. The rules for withholding income tax on wages will be adjusted to reflect this change, but the IRS was given the discretion to leave the withholding unchanged for 2018.

3) Casualty and theft losses. The itemized deduction for casualty and theft losses has been suspended except for losses incurred in a federally declared disaster.

4) Moving expenses. The deduction for job-related moving expenses has been eliminated, except for certain military personnel. The exclusion for moving expense reimbursements has also been suspended.

5) Alimony. Current Rules. Under the current rules, an individual who pays alimony may deduct an amount equal to the alimony or separate maintenance payments paid during the year as an “above-the-line” deduction. (An “above-the-line” deduction, i.e., a deduction that a taxpayer need not itemize deductions to claim, is more valuable for the taxpayer than an itemized deduction.) Also, under current rules alimony and separate maintenance payments are taxable to the recipient spouse (includible in that spouse’s gross income). 2

A. TCJA rules. Under the TCJA rules, there is no deduction for alimony for the payer. Furthermore, alimony is not gross income to the recipient. So, for divorces and legal separations that are executed (i.e., that come into legal existence due to a court order) after 2018, the alimony-paying spouse won’t be able to deduct the payments, and will pay tax on income which generated the alimony. The alimony-receiving spouse doesn’t include them in gross income or pay federal income tax on them.

B. TCJA rules don’t apply to existing divorces and separations. It’s important to emphasize that the current rules continue to apply to already-existing divorces and separations, as well as divorces and separations that are finalized before 2019.

C. Some taxpayers may want the TCJA rules to apply to their existing divorce or separation. Under a special rule, if taxpayers have an existing (pre-2019) divorce or separation decree, and they have that agreement legally modified, then the new rules don’t apply to that modified decree, unless the modification expressly provides that the TCJA rules are to apply. There may be situations where applying the TCJA rules voluntarily is beneficial for the taxpayers, such as a change in the income levels of the alimony payer or the alimony recipient.

6) Like-Kind Exchanges. In a like-kind exchange, a taxpayer doesn’t recognize gain or loss on an exchange of like-kind properties if both the relinquished property and the replacement property are held for productive use in a trade or business or for investment purposes. For exchanges completed after Dec. 31, 2017, the TCJA limits tax-free exchanges to exchanges of real property that is not held primarily for sale (real property limitation). Thus, the benefit of tax-free exchanges of personal property has been eliminated.

As you can see from this overview, the TCJA affects many areas of taxation, and does not necessarily result in less income tax paid for all taxpayers. If you wish to discuss the impact of the law on your particular situation, please give us a call.

__________________________

1 Unless otherwise noted, the changes are effective for tax years beginning in 2018.

2 Please note that the tax rules for child support—i.e., that payers of child support don’t get a deduction, and recipients of child support don’t have to pay tax on those amounts—is unchanged